“I don’t care what you have to do.

If it means walking everywhere and not eating anything that wasn’t purchased with a coupon…

Find a way to get your hands on $100,000.”

You know who said that?

Famous billionaire Charlie Munger, Warren Buffett’s former right hand man.

The first $100,000 is a major milestone in your wealth-building journey.

It’s not easy.

As Charlie Munger said:

“The first $100,000 is a bitch, but you gotta do it.”

And if ‘ol Charlie is using expletives like that, there’s gotta be something to it right?

Today I’ll show you why the first $100,000 is such a big deal…

And how you can build your first $100,000 portfolio before you hit 35.

How to 10X Your Money By Sitting on Your Hands

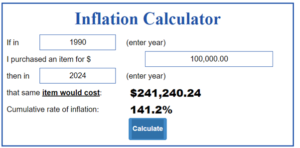

Keep in mind, Charlie talked about your first $100,000 back in 1990…

So the real number today is closer to $240,000.

That’s the bad news.

The good news is once you get your first $100,000 together, your journey to riches becomes infinitely easier.

It’s all because of the power of compounding.

Warren Buffett called it the “eighth wonder of the world.”

You’ve probably heard about it a million times by now…

But once you actually see it in your own portfolio – it can be life-changing.

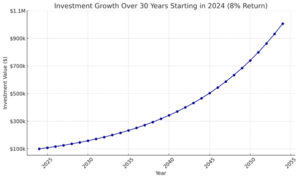

Just take a look at this…

Source: wealthfp.com

Assuming an annual 8% return…

If you wait 30 years and put the power of compounding to work…

Your $100,000 portfolio is now worth $1,006,265,60.

In other words, you 10Xed your money by doing diddly squat!

Now, I know what you’re thinking.

“But Pete, I can’t wait 30 years… I want to be a millionaire NOW!”

Look, I get it.

30 years is a long time to be a millionaire – which isn’t even all that much money anymore these days.

But that’s an extremely conservative example.

It assumes you’re putting your money in the S&P 500 – one of the safest, most conservative investments out there.

You can do a lot better than that too.

Let me give you an example…

Double Your Networth in 12 Months???

I’m on track to make about $110,000 this year.

I’ll put about $20,000-$25,000 of that in savings, about a 20% savings rate – not bad.

But through some wise decisions (and some dumb luck) I’ve also managed to run up about $100,000 in crypto gains this year.

It’s really not that hard when Bitcoin is up about 100% YoY…

And other shitcoins have gone up much higher.

So think about that…

It took me about five years to save up my first $100,000.

I had to work hard, budget, save… all that jazz.

But the next $100,000 fell into my lap in just ONE year – without lifting a finger.

In other words, you can speed up the process 5X without lifting a finger!

Are you starting to see why ole’ Charlie was so adamant about getting your first $100,000 together?

And the earlier you get started, the more you get to take advantage of the power of compounding.

So how do you get there?

Step #1 – Get paid

First things first, you need to make money…

As much as possible.

Sounds obvious I know.

But you can’t save your way to riches when you’re making minimum wage.

That’s why I highly suggest you get your income up to six figures.

Maybe that seems a lot to you right now.

But you’re reading this post right now.

That means you speak english and you have an internet connection.

And I truly believe everybody who has that can hit six figures nowadays.

The key is to build a high-income skill and then get paid.

That could be:

- Copywriting

- Sales/Marketing

- Software/Web development

- Data/AI engineering

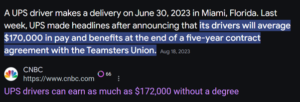

Heck, if you’re blessed enough to be American (lucky bastard!), you could make six-figures driving a UPS truck.

So there’s no excuse.

Get your income to $100k asap.

And start stacking that quap.

That brings us to the next step…

Step #2 – Live Below Your Means

Making $100k is not the same as keeping $100k.

This is where most – especially younger guys – fumble the bag.

They start touching some money and immediately blow it all on expensive cars… fancy designers… designer clothes and other stupid crap.

Listen: You’re not impressing anyone. Nobody cares.

All you do is attract the wrong type of attention.

The smart move is to always live well below your means.

You should aim for a savings rate of at least 15-20%.

The higher the better.

That doesn’t mean you have to become a coupon-clipping tightwad

(although it worked for Warren Buffett, he was such a cheapskate his family had to do an intervention in his 30s)

But be smart with your money.

Spend it wisely.

I personally use a budgeting app called Toshl to track all my expenses and make sure I come out ahead every month.

If you manage to save up $25k every year, you can hit your goal in just four years…

And that’s not even accounting for capital gains / dividends – remember the whole power of compounding and all that?

That brings us to the final step…

Step #3 – Put that Money to Work

According to the Bureau of Labor Statistics, consumer prices have soared 21% since 2020.

In other words, your cash has lost 21% in value!

You do NOT want to have your money rotting away in a bank account.

Personally, I have $10,000 in my bank account for expenses.

Everything else is deployed.

I’ll write a separate post on my investments strategy later…

But I suggest you stick with T-bills (low risk-low reward)… Stocks (medium risk-medium reward)… and Crypto (high risk-high reward).

Let me briefly go into each of these.

T-Bills

Let’s start with the boring boomer investment first.

T-bills are short-term government debt.

In other words, they’re backed by the US Government.

And they pay about 4.5% interest right now.

It doesn’t get much safer than that…

And you get paid every month.

You can easily buy them from the US treasury (home.treasury.gov) or through mutual funds like:

- Schwab Treasury Obligations Fund (SYM:SNOXX)

- Fidelity Treasury Money Market Fund (SYM:FZXFXX)

- Vanguard Federal Money Market Fund (SYM:VMFXX)

So make sure you take advantage.

Stocks

According to S&P Global, 9 out of 10 professional money managers can NOT outperform a single index.

These are Wall Street sharks that manage investments for a living.

You think you can do better?

Maybe… but I highly suggest you start off by playing it safe.

Just buy a broad-market index fund tracking the S&P 500 like SPY or VOO…

Or a global ETF like MSCI.

Both have historically returned about 10% per year… throughout busts and booms.

So you can’t go wrong with those.

Once you have built up major positions in ETFs you can expand by buying single stocks.

But again, I highly suggest you keep it simple.

It’s not sexy… it’s not exciting… but it works.

Speaking of sexy and exciting.

Crypto

Now crypto is a real rollercoaster where fortunes can be made (and lost) in the blink of an eye…

If you’re younger and serious about building wealth, you can’t afford to ignore crypto.

But don’t go crazy and gamble all your money some random shitcoin you saw on twitter.

Again, play it safe.

But the majority of your crypto position in BTC.

That’s the big dawg and as safe as crypto can get.

Same principle as in stocks…

Keep the biggest part of your holdings in BTC…

And feel free to place smaller bets on ultra-risky shitcoins.

You can even buy BTC ETFs through your stock brokerage now.

HODL… IBIT… BTC….

There are countless options.

Conclusion (tl;dr)

That’s it.

To sum it all up:

- Learn a high-income skill and build a six-figure income

- Track your expenses, live below your means and stack cash every month

- Put your money into T-Bills, stocks and crypto

Simple, no?

Follow these three steps and you’re well on your way to your fist $100,000 portfolio.

Which is the foundation for real wealth down the road.

I believe anyone with a modicum of drive, discipline and intelligence can hit this goal in a few years.

What’s important is that you start NOW.

So let’s get it.

If you have questions or think I’m missing anything, let me know in the comments below.

Good luck and Godspeed.